Expand Briefing

AI Systems | Digital Infrastructure | AI Infrastructure | Semiconductors

2026-06-10 · Framework Essay

2026-06-10 · Framework Essay

When NVIDIA reported fiscal 2026 revenue of $215.9 billion — up 65% from the prior year — with a GAAP operating margin above 60%, it confirmed something the market had already started to price: one company had captured a disproportionate share of the economics from an industry-wide buildout. The GPU was the entry point. The software stack was the moat. Customers had no real alternative.

That story is clean and compelling. The problem is what happened next: the same logic got applied to every company with an "AI" label attached. The assumption, rarely stated but widely held, was that AI infrastructure demand is a kind of rising tide — and that relevance to the tide is enough to determine how much water each company gets.

It isn't.

The core issue is a category mistake. "AI exposure" describes where a company sits relative to a theme. It says nothing about what the theme does to that company's economics once it arrives. Those are different questions, and collapsing them produces bad analysis.

Consider what actually happens when AI infrastructure spending expands and moves down the value chain.

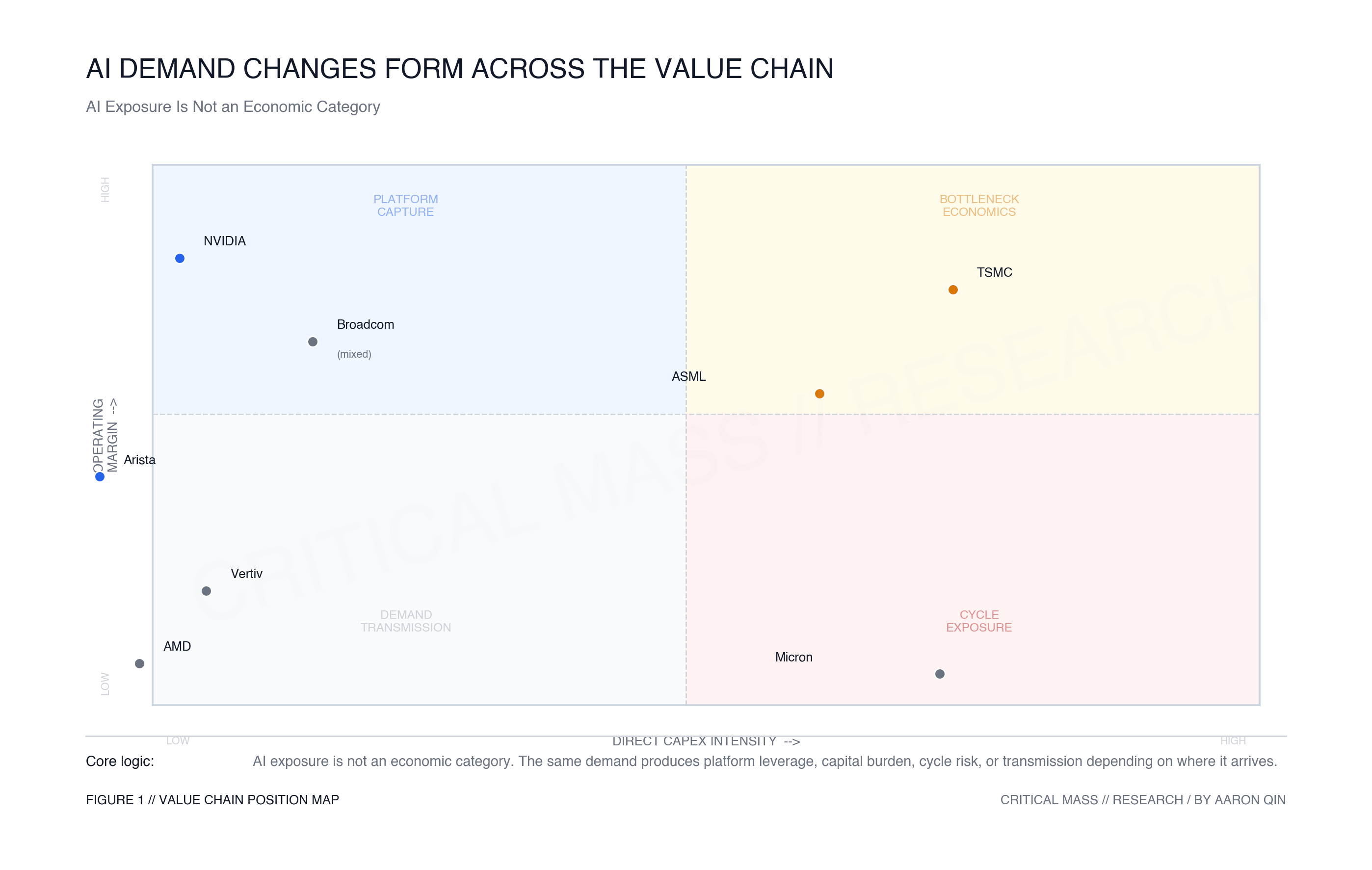

At NVIDIA, demand arrives as platform leverage. The company designs chips but does not build fabs. Its direct capital expenditure runs at roughly 2-3% of revenue. When data center orders increase, operating income expands faster than costs because incremental revenue flows through a software-defined platform where the marginal cost of an additional customer is low. The operating margin above 60% is not just a reflection of strong demand. It reflects the structure of the business: demand enters a platform and exits as profit, with relatively little capital consumed in between.

At TSMC, the same wave of AI-driven demand arrives in an entirely different form. TSMC has to build the capacity that turns AI chip designs into physical silicon: new fabs, new nodes, CoWoS advanced packaging lines. That requires sustained capital investment running above 30% of revenue. Revenue grows. Margins are strong. But the company is simultaneously reinvesting a large fraction of its income to maintain and extend the manufacturing capability that makes those margins possible. AI demand and capital obligation coexist here — being essential to the system does not mean extracting value from it in the same way NVIDIA does.

Micron is a different case again. High-bandwidth memory is real and strategically important — HBM sits inside the AI accelerators that now define the computing stack. But memory has a structural problem that AI relevance does not automatically dissolve: the business runs in cycles. Pricing corrects. Inventory builds. Capital spending to maintain competitive process technology is heavy and ongoing. Micron's direct CapEx intensity runs at levels comparable to TSMC, but without foundry-style pricing power and with continued exposure to commodity memory dynamics. The HBM narrative improves the story. It does not rewrite the underlying economics.

ASML's role is one step further removed. The company supplies the lithography equipment that enables the fabs that build the chips that run AI workloads. That makes it a genuine bottleneck — without EUV lithography, advanced semiconductor manufacturing stalls. But AI demand reaches ASML indirectly, filtered through its customers' own capital spending cycles. When TSMC and Samsung invest in new capacity, ASML benefits. When those customers pause, ASML feels it first. The margin structure is strong and defensible, but the business model is equipment order cycles and long customer qualification processes, not compute platform leverage.

Move further down the stack and the economics shift again. Arista supplies switching and networking infrastructure for AI clusters. Its margin profile is notable — operating margin above 40%, direct CapEx below 1% of revenue. But that capital-light profile reflects the nature of the business, not an NVIDIA-style platform position. Arista captures value at the networking layer because AI clusters require high-performance networking fabric. Demand passes through that layer because it has to, not because Arista controls the system entry point. That is a real and defensible position. It is not the same position.

Vertiv sits at the physical end of the chain: power distribution, thermal management, liquid cooling. AI data centers are real and growing customers. But Vertiv's gross margin runs around 37% — structurally different from the compute, equipment, or networking layers above it. The business is closer to industrial infrastructure than to semiconductor economics. AI demand reaches Vertiv first as volume, and only later as operating leverage if higher-density power systems, liquid cooling, and service attachment can raise structural margins over time.

The pattern across all of these is not complicated once you look for it: AI demand changes economic form as it moves through the value chain.

At the platform layer, it becomes operating leverage with low capital consumption.

At the manufacturing layer, it becomes revenue alongside capital obligation.

At the memory layer, it improves the narrative while cycle risk persists underneath.

At the equipment layer, it becomes indirect demand filtered through customer investment cycles.

At the networking layer, it becomes capital-light transmission with its own margin structure.

At the facility layer, it becomes volume-driven infrastructure revenue with a different cost base.

At the manufacturing layer, it becomes revenue alongside capital obligation.

At the memory layer, it improves the narrative while cycle risk persists underneath.

At the equipment layer, it becomes indirect demand filtered through customer investment cycles.

At the networking layer, it becomes capital-light transmission with its own margin structure.

At the facility layer, it becomes volume-driven infrastructure revenue with a different cost base.

None of these is the same thing. But all of them get described with the same phrase.

These classifications are not permanent. NVIDIA would become less exceptional if competing accelerator platforms reduced switching costs and compressed margins. Micron would deserve a different reading if HBM mix stabilized pricing across a full memory cycle. Vertiv would move closer to leverage if liquid cooling and high-density power systems raised structural margins rather than simply increasing project volume. ASML would weaken as a bottleneck if customer capacity cycles decoupled from AI demand. The point is not to assign fixed labels, but to test what form AI demand takes at each node — and to update that test as evidence changes.

The analytical implication is straightforward, even if it is easy to forget when a cycle is running hot. "AI exposure" should be the beginning of a question, not its answer. The question it opens is: when AI demand reaches this company, what does it actually become?

Does the business structure convert demand into operating leverage, or absorb it as capital obligation? Is the company's position one that customers are forced to depend on, or one that transmits demand because it happens to sit in the path? Does scarcity support pricing power, or does commoditization cap it?

These questions do not have uniform answers. NVIDIA and Vertiv are both AI infrastructure companies. They are not the same kind of AI infrastructure company. Treating them as if they belong to the same economic category — because they share a label — is the mistake worth being precise about.

This essay is the written layer of the AI Infrastructure Economics analytics module. Issuer-level metrics referenced here are derived from public filings; methodology and data boundaries are documented in the Analytics Methodology page. NVIDIA fiscal 2026 figures are from the company's February 2026 earnings release. All other company metrics reference the fiscal year rows in the current analytics dataset. This is not investment advice.