Expand Briefing

This piece reflects a personal analytical framework based on public information and systems-level reasoning. It is not investment advice.

Overview

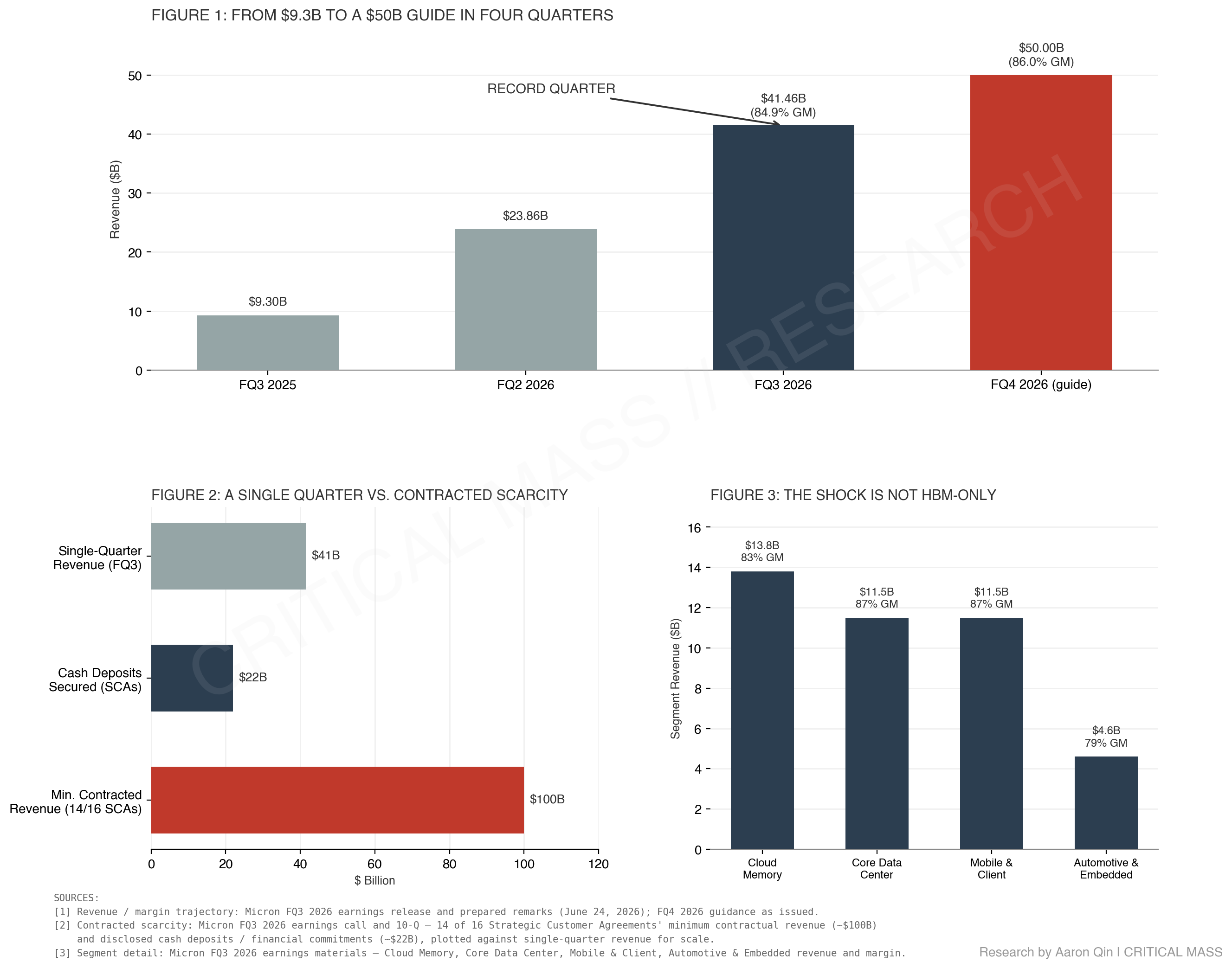

Micron's fiscal Q3 2026 was an abnormal quarter even before the Strategic Customer Agreements are considered. Revenue was $41.46 billion, up from $23.86 billion in the prior quarter and $9.30 billion a year earlier. Non-GAAP gross margin reached 84.9%, and non-GAAP diluted EPS was $25.11. One quarter of revenue exceeded Micron's entire fiscal 2025 revenue base. Micron also guided fiscal Q4 revenue to approximately $50.0 billion, with non-GAAP gross margin near 86%.

That is the visible shock. The more useful question sits underneath it: memory companies have always had violent upcycles, so the interesting test is not how large this one is, but whether it is still behaving like a conventional memory cycle or whether AI demand has introduced a new economic mechanism. Micron's FQ3 evidence points toward the second answer, with a boundary — the memory cycle has not disappeared, but part of it has become contracted.

The quarter is best read as a contract event, not only a margin event.

From compute demand to memory dependency

AI infrastructure is usually priced through compute — GPUs, accelerators, and training clusters remain the visible layer of the story. Micron's quarter shows the constraint moving deeper into the system.

Micron's own framing is direct: AI systems can be built around GPUs, ASICs, or CPUs from different suppliers, but they share one architectural dependency, since system performance depends on memory subsystem capacity and bandwidth. That dependency has elevated memory from a component input into a strategic asset.

The distinction changes the form of demand. If memory is only a commodity component, customers can buy it through the cycle as needed. If memory is a system constraint, customers have to reserve it before the system exists at full scale — which is closer to what Micron's FQ3 disclosure describes.

The supply constraint is physical, not narrative

Micron's supply argument is not only that demand is strong. It is that supply cannot respond normally.

The company expects tight DRAM and NAND conditions to persist beyond calendar 2027. Even with gradual supply improvement expected in 2028, Micron said it does not yet have line of sight to when memory supply will catch up with increasing demand. The stated constraints include greenfield fab lead times, shortages of skilled trade labor, permitting complexity, energy infrastructure, rising process complexity, slower bit growth from technology transitions, larger cleanroom requirements, and HBM's rising trade ratio pressuring non-HBM supply.

Memory supply is not software capacity — it is built through fabs, cleanrooms, tools, power, materials, process transitions, and advanced packaging, on timelines measured in years, not quarters. When supply cannot flex on the same timeline as demand, customers stop treating memory as a disposable input and start treating it as capacity that has to be reserved ahead of use.

The hard evidence is commitment

Micron has signed 16 Strategic Customer Agreements, or SCAs, across data center, consumer, and automotive customers. These agreements typically run for five years, from calendar 2026 through the end of calendar 2030, while automotive agreements generally run for three years. The 16 agreements cover roughly 20% of Micron's DRAM volume and about one-third of its NAND volume over the period.

The structure matters more than the count. The SCAs are take-or-pay agreements with binding volume commitments. The largest agreements generally use the current calendar Q2 market price as a ceiling for existing products while setting a floor price through the term of the agreement. For agreements with price bands, Micron says the floor price supports gross margins well above the company's peak quarterly margins in any past cycle.

Fourteen of the 16 signed SCAs carry cumulative minimum contractual revenue of approximately $100 billion over the remaining agreement terms — the same figure Micron separately discloses as remaining performance obligations (see below), described from the revenue-commitment side rather than the accounting side. Micron also expects $22 billion of cash deposits and related financial commitments from the SCAs signed so far, including roughly $18 billion in cash deposits.

Demand can be a forecast, guidance, or management language. Take-or-pay terms, volume commitments, price floors, and deposits are a different kind of evidence: they are enforceable.

RPO changes the evidence, not the whole model

Micron's 10-Q gives the accounting version of the same shift. The company describes the SCAs as take-or-pay agreements with binding commitments for specific volumes over multi-year contract terms. Most agreements have pricing that is either fixed or subject to minimum and maximum pricing; a minority of agreements do not have fixed pricing or price bands and remain subject to market conditions.

As of FQ3 end, Micron disclosed roughly $5 billion of remaining performance obligations. Including agreements executed after quarter-end, RPO for SCAs signed so far was approximately $100 billion. Micron cautioned that this RPO figure is based on minimum committed volumes and minimum pricing, and is not indicative of total future revenue under the contracts.

That boundary is worth taking seriously: the $100 billion figure is a floor-based accounting view, not a full backlog model. But it still changes the evidentiary quality of the demand claim. Memory demand is no longer visible only through shipments and ASPs — part of it is now visible through enforceable customer commitments.

Scarcity is spreading beyond HBM

The quarter was not only an HBM data-center event. DRAM revenue was $31.3 billion, 76% of total revenue, and grew 67% sequentially; DRAM bit shipments increased only in the low-single-digit percentage range, while ASPs increased in the low-60s percentage range. NAND revenue was $9.9 billion, 24% of total revenue, and grew 99% sequentially; NAND bit shipments increased in the mid-single-digit percentage range, while ASPs increased in the mid-80s percentage range.

The business-unit data show the same pattern: Cloud Memory revenue was $13.8 billion at 83% gross margin, Core Data Center was $11.5 billion at 87%, Mobile and Client was $11.5 billion at 87%, and Automotive and Embedded was $4.6 billion at 79%.

If this were only an HBM story, the pricing shock would be concentrated in one reporting unit. Instead it shows up across data center, client, mobile, and automotive and embedded markets — evidence that AI infrastructure demand is not just adding HBM revenue, but tightening the memory market around it.

Economic distribution

The economics of the quarter separate into four questions.

Who captures value? Micron, through tight supply, higher ASPs, premium product mix, price floors, and contracted volume.

Who bears cost? Customers, through take-or-pay commitments, cash deposits, and supply-assurance premiums. Reuters described the shift directly: AI-driven shortages are forcing large-scale data-center customers to fund capacity, reshaping the memory market.

Who controls the bottleneck? Not HBM as a single product, but advanced DRAM, NAND, cleanroom allocation, process-node transitions, HBM packaging, and long-term access to supply more broadly.

Who carries risk? Micron still carries capex execution risk and future supply-normalization risk. The company reported $7.1 billion of net capital expenditures in FQ3 and guided toward approximately $27 billion of fiscal 2026 capital spending, with fiscal 2027 quarterly capex expected to exceed fiscal Q4 levels as the company pulls in cleanroom capacity. Contracted demand can justify that spending. It cannot build the fabs on its own.

The countercase: memory is still cyclical

The bear case is not complicated. If capacity arrives faster than expected, pricing power weakens. Reuters reported that Micron's bull case depends on tightness holding, and that pricing power is the first thing at risk once supply begins to return; Reuters also noted that system designs using cheaper memory could limit how much premium pricing can persist.

Micron's own risk disclosures preserve the same boundary: if worldwide memory and storage supply increases faster than demand, average selling prices can fall and materially affect the business. The company also identifies construction execution risk, equipment availability, labor, materials, services, power, and other infrastructure dependencies as constraints on its own expansion.

The right conclusion, then, is narrower than "the cycle is over." Micron has contracted part of the current scarcity ahead of the next supply response — not replaced the cycle with something permanent.

Why the GM agreement matters

Update, July 1, 2026: Micron and General Motors announced a Strategic Customer Agreement on July 1 — after this note's original June 27 publication date — covering long-term supply of memory and storage platforms for GM's next-generation vehicles. The section below was added at that time; everything above reflects the original FQ3 analysis.

GM secured long-term supply of Micron memory and storage platforms for future vehicle production, and the two companies agreed to collaborate on future memory and storage technology requirements. Micron tied the agreement to its U.S. manufacturing expansion, including the modernization of its Manassas, Virginia fab. Reuters reported that GM characterized the deal as a precautionary measure to shore up access to key components, not a reaction to any current supply problem — and that it was one of the 16 SCAs Micron had already outlined on its FQ3 call.

The example is useful because it shows SCA demand is not only a hyperscaler phenomenon. AI data-center demand tightens the upstream memory market, but the supply-assurance response is now visible in automotive too, where product lifecycles are long and component continuity matters more than spot pricing.

Conclusion

Micron's FQ3 2026 does not settle the memory-cycle question. It sharpens it.

The financial results are the visible shock: record revenue, extreme margins, and a Q4 outlook above the record just reported. The more durable evidence is contractual — multi-year SCAs, take-or-pay commitments, pricing floors, customer deposits, and RPO disclosure that makes part of the demand claim enforceable rather than merely stated.

That does not make Micron non-cyclical. It does make the current cycle harder to analyze using spot pricing and quarterly shipments alone. The memory cycle is still visible — but part of it is now contracted scarcity.

Sources and notes

- FQ3 2026 Earnings Release and Guidance: Micron fiscal Q3 2026 earnings release and prepared remarks, June 24, 2026 — basis for the $41.46 billion revenue figure, non-GAAP gross margin and EPS, and the fiscal Q4 guidance (~$50 billion revenue, ~86% gross margin).

- Strategic Customer Agreements Structure: Micron FQ3 2026 earnings call and presentation materials — basis for the count (16 SCAs), term lengths, take-or-pay structure, price-floor/ceiling mechanics, the ~$100 billion minimum contractual revenue figure, and the $22 billion cash-deposit and financial-commitment figure.

- Remaining Performance Obligations Disclosure: Micron fiscal Q3 2026 Form 10-Q — basis for the ~$5 billion RPO reported as of quarter-end, the ~$100 billion RPO figure including agreements signed after quarter-end, and Micron's own caution that RPO reflects minimum committed volumes and pricing rather than total expected revenue.

- Segment and Product Line Detail: Micron FQ3 2026 earnings materials — basis for the DRAM/NAND revenue split, bit-shipment and ASP growth ranges, and the business-unit revenue and margin figures (Cloud Memory, Core Data Center, Mobile and Client, Automotive and Embedded).

- Market Interpretation of Supply-Funding Shift: Reuters coverage of Micron's FQ3 2026 results — basis for the framing that AI-driven shortages are pushing data-center customers to fund capacity directly, and for the bear-case framing that pricing power is most exposed once supply returns.

- Micron-GM Strategic Agreement: Micron and General Motors joint announcement and Reuters coverage, July 1, 2026 — basis for the GM supply agreement, its tie to the Manassas, Virginia fab modernization, and GM's characterization of the deal as precautionary rather than reactive; added to this note after its original publication date.